The Department of the Treasury and the IRS on March 5 released final regulations (TD 9988) on the elective pay election for certain energy tax credits under IRC Section 6417, added by the Inflation Reduction Act (IRA), which treats the credits as a payment against federal income tax liabilities.

The Department of the Treasury and the IRS on March 5 released final regulations (TD 9988) on the elective pay election for certain energy tax credits under IRC Section 6417, added by the Inflation Reduction Act (IRA), which treats the credits as a payment against federal income tax liabilities.

The final regulations adopt the proposed regulations (REG-101607-23) with some modifications that clarify which applicable entities are eligible to make an elective pay election and how the election should be made.

The IRS also updated the elective payment frequently asked questions based on the final regulations. Finally, the IRS issued Notice 2024-27, which requests additional comments on any situations in which an elective payment election could be made for a clean energy credit that was purchased in a transfer, a sequence of events referred to as chaining.

Background

The IRA introduced, for tax years beginning after December 31, 2022, the ability for some entities to monetize applicable tax credits via an “elective pay” election under IRC Section 6417. This allows applicable entities to treat certain credits as payment against their federal income tax liabilities and to receive a refund of any excess payment.

Eligible Credits and Entities

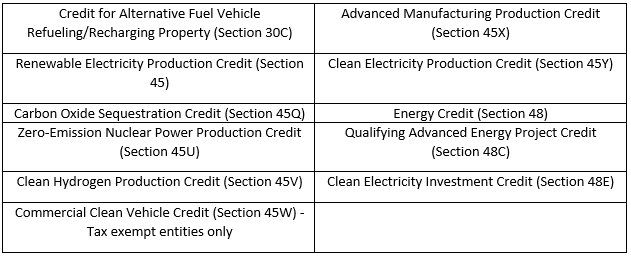

The IRA specifies that only some credits and entities as eligible for the elective pay election under Section 6417. Applicable credits include:

Eligible entities, referred to as “applicable entities,” include:

- Tax-exempt organizations

- Any state, the District of Columbia, or political subdivision

- An Indian Tribal government or subdivision

- Any Alaska Native Corporation

- The Tennessee Valley Authority

- Rural electric cooperatives

- An agency or instrumentality of certain applicable entities

Partnerships

While the final regulations bring clarity to the issue of determining which entities are eligible to make an elective pay election, they notably exclude partnerships from making such an election (except with respect to Section 45V, 45Q, and 45X credits). This exclusion has significant implications for the renewable energy sector, where projects are commonly structured as partnership entities to pool capital, diversify risk, and combine the expertise of various entity partners.

During the comment period on the proposed regulations, several commenters advocated for the inclusion of mixed partnerships – that is, partnerships that consist of both applicable entity and non-applicable entity partners -- as applicable entities to allow for an elective payment election equal to the applicable entity partner’s allocable credit. However, Treasury and the IRS rejected those suggestions and adopted the regulations as originally proposed.

However, the final regulations do allow entities to make a valid election out of Subchapter K as a means for these entities to make an elective pay election. Feedback from commenters highlights the complexities and burdensome requirements that arise from making such an election out of Subchapter K, limiting its usefulness. Treasury and the IRS acknowledged such challenges and simultaneously issued proposed regulations under Section 761 for renewable energy projects that validly elect out of Subchapter K. Under the proposed regulations, exceptions would allow certain unincorporated organizations to make an elective pay election.

Tax-Exempt Grants & Loans

The final regulations adopt special rules regarding qualified energy property acquired using certain tax-exempt grants and forgivable loans. The rules state that (1) tax-exempt amounts are includable in the basis of the property and (2) “no excess benefit” can be derived from the use of restricted tax-exempt amounts used towards acquiring investment-related credit property.

The addition of the “no excess benefit” rule effectively limits the amount of the applicable credit that can be claimed such that the sum of any restricted tax-exempt amount(s) and the applicable credit does not exceed the cost of the investment-related credit property. This rule applies only to tax-exempt amounts that are restricted for the specific use of purchasing, constructing, reconstructing, erecting, or acquiring investment-related credit property. The final regulations include examples to illustrate this rule.

Making the Election

To participate in the elective pay election, all credits must undergo a prefiling registration process and the applicable entity must secure a valid registration number. Credits can be registered as early as the first day of the taxable year in which the qualified energy property is placed in service. Any election received by the IRS without a valid registration number will be deemed ineligible. As currently established, a “short form” renewal process for multiyear credits such as the production tax credit is not available. A new registration must be submitted each year a credit is generated.

Applicable entities that already file an annual tax return would continue to file that return with the appropriate tax credit form and Form 3800 completed. Applicable entities that do not file an annual information return with the IRS would utilize Form 990-T. Note that the elective pay election must be made on an originally filed return (including extensions) and cannot be made on an amended return.

The final regulations also confirm that fiscal year organizations that do not normally have tax filing requirements may adopt a tax year-end different from its current accounting year-end. Such organizations are required to maintain adequate books and records of any differences between its normal fiscal year-end books and adopted tax year-end books. This provides increased opportunity for organizations that placed qualified energy property in service early in 2023 and otherwise would have been excluded from a tax credit benefit.

Processing of Payments

Treasury and the IRS opted not to define a specific time frame for processing payment of an elective pay election, instead indicating in the preamble that the prefiling registration process is designed to verify certain limited information in advance and mitigate the risk of delayed payment processing by the IRS.

The final regulations additionally confirm that applicable entities that choose to make this election will receive payment in one lump sum as opposed to multiple payments. Some commenters had suggested an accelerated payment mechanism that would enable applicable entities to submit the election as early as the placed-in-service date of the qualified energy property, thus enabling the IRS to provide pre-payment of a portion of the applicable credit based on a review of the prefiling registration information. Given that the elective payment amount is treated as made when a credit claim or the annual tax return is filed, Treasury and the IRS concluded that it would not be possible to implement this mechanism.

For more information about the above article or other business tax services, contact Lesley L. Price, CPA, by calling (334) 887-7022 or by leaving us a message below.

Written by Leah Turner, Aaron Wright and Gabe Rubio. Copyright © 2024 BDO USA, P.C. All rights reserved. www.bdo.com