Since the outbreak of COVID-19, the restaurant industry has been one of the hardest hit by the pandemic’s impacts, leading to spikes in business closures, continued capacity limitations, and unprecedented loss in both jobs and sales. However, many establishments were able to keep their doors open and continue to serve customers throughout the course of the pandemic with the help of federal aid issued through the CARES Act programs, Restaurant Revitalization Fund, and other relief programs. As a result, restaurants may be subject to the Single Audit this year.

Since the outbreak of COVID-19, the restaurant industry has been one of the hardest hit by the pandemic’s impacts, leading to spikes in business closures, continued capacity limitations, and unprecedented loss in both jobs and sales. However, many establishments were able to keep their doors open and continue to serve customers throughout the course of the pandemic with the help of federal aid issued through the CARES Act programs, Restaurant Revitalization Fund, and other relief programs. As a result, restaurants may be subject to the Single Audit this year.

Before approaching your Single Audit, consider the following to ensure you comply with your federal relief program:

1. Confirm whether you’re subject to the Single Audit. The Single Audit is a financial statement and compliance audit designed to ensure businesses comply with their federal award program, according to the Office of Management and Budget’s (OMB) Uniform Guidance. Any restaurant that spends at least $750,000 in federal funds in a fiscal year is required to undergo a Single Audit. Programs that could trigger a review include the Coronavirus Relief Fund (CRF), Restaurant Revitalization Fund, and others.

However, federal award programs have varying requirements. You should be sure to check the guidance outlined in your financial package and speak with a professional to determine if you’re subject to the Single Audit.

2. Understand what’s required of the audit. The Single Audit is divided into two parts: the financial statement audit and the compliance audit. The financial statement audit is performed in accordance with both generally accepted accounting standards (GAAS) and government auditing standards (GAS) to report on internal controls and compliance with laws and agreements. The compliance audit assesses whether a restaurant is adhering to the terms of its federal awards.

“Major programs” identified by the OMB’s Uniform Guidance are determined by an independent auditor and are subject to the compliance audit.

3. Perform an internal assessment ahead of your official audit. Before contacting a third-party auditor, you should assess your operations and documentation to ensure you comply with the requirements of your federal program. Conduct a gap analysis to identify areas where your internal controls don’t align with the federal requirements so that you can make appropriate adjustments before year-end. The auditor will not only examine the execution of your internal controls but also their design and implementation to assess whether they perform as they’re intended to.

Collect all relevant documentation that provides evidence of the proper use of your financial relief and, ultimately, the completion of the Single Audit. If you’re unsure which documents will best support your compliance, review the guidelines of your federal awards package.

Lastly, if you have passed funds along to other organizations, be sure any sub-recipient relationships you have in relation to your federal awards also adhere to the federal program requirements. This is particularly relevant for any restaurants that have shared federal funding with partnering companies. Restaurants that share financial relief with another establishment are subject to the risks of the “sub-recipient” restaurant if they’re found non-compliant.

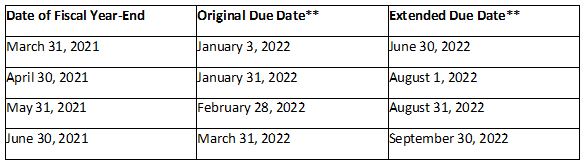

4. Stay up to date on deadline extensions. Since COVID-19’s outbreak, there have been a number of extensions for reporting the Single Audit. In the latest update issued in March 2021, organizations that hadn’t yet filed and have fiscal years through June 30, 2021, now have six more months to file after their initial due date.

Examples of Extensions by Fiscal Year:*

*The Office of Management and Budget has not clarified the guidance and the effect on entities who may be late on their filing and the effect on the determination of low-risk auditee for the next year’s audit.

**Per the Uniform Guidance, if the due date falls on a Saturday, Sunday, or Federal holiday, the reporting package is due the next business day. Dates in these columns have been adjusted accordingly.

The Single Audit can be complex, especially for first-time applicants, and there are a number of other factors that can assist your restaurant in ensuring a successful review. Whether or not your establishment is subject to the Single Audit, it is imperative that you maintain adequate documentation of your expenses against federal relief and comply with all of your programs’ requirements, as a federal agency may still request to examine your books and records and supporting documentation for federal expenditures.

For more information on the above article or any audit & assurance services, contact Melissa Motley, CPA, at (334) 887-7022 or by leaving us a message below.